Estimated Chargeable Income (ECI) of Your Singapore Company

Estimated Chargeable Income (ECI) reflects your company’s estimated taxable profits for a specific financial year. All Singapore companies must prepare and file their ECI report with the Inland Revenue Authority of Singapore (IRAS) unless they meet the exemption criteria.The ECI must be filed within three months (90 days) from the end of the company’s financial year.

In this article, we will explore the essential aspects of ECI, including how to determine if your company needs to file and detailed guidance on calculating and submitting your ECI accurately. Additionally, we’ll provide practical tips to help you avoid common mistakes, ensuring a smooth and hassle-free filing process.

This article includes the following topics:

Estimated Chargable Income (ECI), Tax Assessment, and Tax Return Filing Explained

Compared to many other jurisdictions where companies are only required to submit annual tax returns, the IRAS is under a slightly different system, as explained below.

1. Submit ECI within 90 days

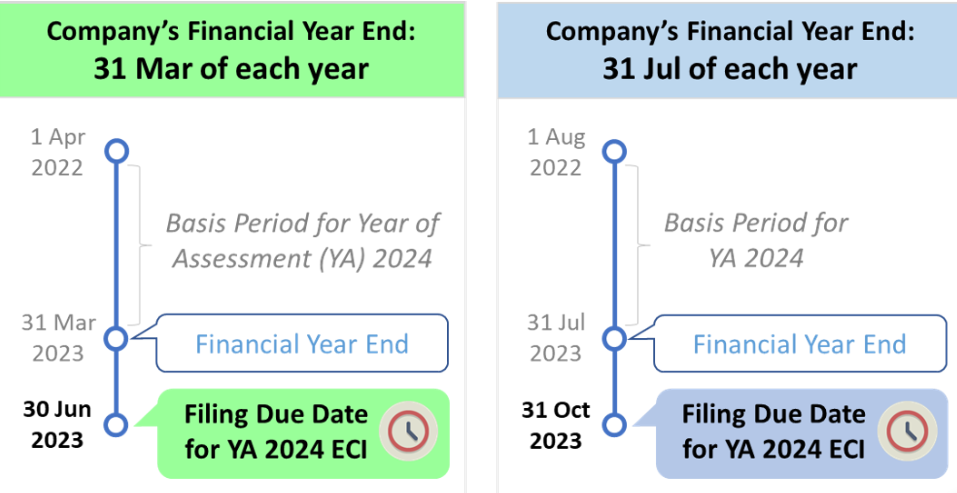

The ECI is an estimate of a company’s taxable profits for a specific financial year. It represents a simplified calculation of the company’s taxable income serving as a forecast of the company’s taxable profits for that year. The ECI must be filed within three months of the end of the financial year (e.g., if your financial year ends on 31 December 2023, the ECI must be submitted by 31 March 2024). The filing of ECI provides the Inland Revenue Authority of Singapore with an early estimate of the company's tax liability and allows them to send you a preliminary tax assessment.

2. Receive Tax Assessment from IRAS

After the ECI is submitted, IRAS reviews it and issues a Notice of Assessment (NOA), which states the amount of tax payable based on the declared ECI. If a company files a nil ECI (indicating no taxable income), IRAS will not issue an NOA. However, if chargeable income is declared, the company must pay the estimated tax within one month of receiving the NOA.

3. File Tax Return

The tax return is a more detailed report of the company’s actual taxable income for the financial year, filed through Form C-S, C-S (Lite), or Form C. This filing reflects the company's final chargeable income after accounting for deductible expenses, capital allowances, and tax-exempt amounts. Unlike the ECI, tax returns provide a comprehensive breakdown of the company’s financial activities. Companies have more time to file these forms, with the deadline falling on 30 November of the year that follows the year of the financial year in question (e.g., if the financial year ends anytime in 2023, the tax return must be submitted by 30 November 2024).

4. Reconciliation of ECI and Final Tax Return

After the final tax return is filed, IRAS compares it with the previously submitted ECI:

- If the actual chargeable income is lower than the ECI: The company will receive a refund for any overpaid tax.

- If the actual chargeable income is higher than the ECI: The company must pay the additional tax within one month of receiving the new NOA.

Overall, this approach offers several key benefits to both the companies and the IRAS in the following ways:

a. Early Revenue Collection for IRAS

Since ECI must be filed within 90 days of the company’s financial year end, it allows IRAS to collect revenue early in the financial year. Thus, IRAS can anticipate tax receipts earlier, which improves financial forecasting and ensures sufficient liquidity for public expenditure.

b. Smoother Cash Flow Management for Companies

When a company files its ECI, it can opt to pay its taxes through monthly installments rather than a lump sum. This eases the financial burden on companies by allowing them to spread their tax payments over several months.

c. Allows Companies More Time to Finalize Their Tax Returns

Filing the ECI provides companies with the flexibility to estimate their tax liabilities based on preliminary financial data while allowing more time to finalize detailed and accurate financial statements and tax returns. Since companies only need to provide an estimate within three months of the financial year-end, they can use the remaining time to thoroughly review, audit, and finalize their complete tax return (Form C or Form C-S).

Who Needs to File ECI in Singapore?

Subject to certain exceptions as described below, all Singapore-incorporated companies are required to file their Estimated Chargeable Income within three months from the end of their financial year.

There are two key scenarios in which a company may not need to file ECI:

ECI Filing Exemption: Who Qualifies and the Benefits

Your company may qualify for an ECI filing waiver if it meets both of the following criteria for the given financial year:

- Annual Revenue is S$5 Million or Below: The company’s revenue, which refers to its main source of income, must be S$5 million or less for the financial year. Revenue excludes separate income sources such as interest, dividends, and rental income, which do not arise from the company’s principal activities. For investment holding companies, revenue is defined as income from investments, such as dividends and interest.

- Nil Estimated Chargeable Income: The company’s ECI must be nil for the Year of Assessment. It’s important to note that ECI should be calculated before deducting any exempt amounts under schemes like the partial tax exemption or the tax exemption for new start-up companies.

If your company meets both of these criteria, it is not required to file an ECI for that YA. However, if only one condition is met, the company will still be required to file the ECI. It is your responsibility to self-assess whether your company qualifies for the waiver, and there is no need to seek approval or notify the Inland Revenue Authority of Singapore.

Entities Specifically Not Required to File ECI in Singapore

Certain entities are exempt from the requirement to file ECI, even if they do not qualify for the above ECI filing waiver criteria. If your company falls into one of the following categories, it is not required to file ECI:

- Foreign Ship Owners or Charterers: Companies in this category do not need to file ECI if their local shipping agent submits the Shipping Return on their behalf.

- Foreign Universities: Educational institutions operating as foreign universities are exempt from filing ECI.

- Designated Unit Trusts and Approved CPF Unit Trusts: Specific unit trusts that are designated or approved by the Central Provident Fund (CPF) are not required to file ECI.

- Real Estate Investment Trusts (REITs): REITs that have been granted tax treatment under Section 43(2) of the Income Tax Act 1947 are exempt from filing ECI.

- Specially Waived Cases by IRAS: In certain situations, IRAS may specifically grant a waiver for a company, exempting it from filing ECI.

How to Calculate ECI?

Your in-house accountant or your external tax agent should be able to handle the calculation, prepare filing data in the relevant format, and file it with IRAS.

As the corporate services provider for companies that are under our administration, we generally handle the tax filing for all our portfolio companies.

How to File Estimated Chargable Income (ECI)?

Your company is required to file its ECI within three months (90 days) from the end of its financial year.

Typically, IRAS will send your company a notification to file its ECI during the last month of your financial year. However, even if your company does not receive this notification, it is mandatory to file the ECI within the specified three-month period, unless the company meets the exemption criteria.

See below the examples of ECI Filing Due Dates:

We Have Helped Thousands Incorporate In Singapore

Late Filing or Failure to File ECI in Singapore

Consequences of Late or Non-Filing

1. Estimated Notice of Assessment

If your company fails to file ECI on time, IRAS may issue an estimated Notice of Assessment. This assessment is based on your company’s historical financial data or any other information that IRAS has on record.Your company is required to pay the full tax amount specified in this notice within one month from the date of the assessment. Unlike timely filers, your company will not be eligible for installment payments and must settle the amount in full.

2. Penalties

General non-compliance can lead to fines up to S$5,000 or 3 years imprisonment. For those with the intention to evade taxes, the penalties can get up to 400% of the undercharged tax and a S$50,000 fine or 5 years imprisonment.

However, it’s important to note that such penalties are rare for companies that operate in good faith, especially those that use the services of professional tax agents. By staying compliant and seeking expert guidance, most companies can avoid these severe consequences.

Protect Your Income From Excessive Taxation

How We Can Help

Related Articles

Is Singapore the Right Place to Incorporate?

How to Register a New Company in Singapore

Singapore's Tax System and Types of Taxes