Corporate Services in Singapore: Incorporate with the Right Partner

Starting a new company can feel complex. It doesn't have to be. Our experienced, ACRA-licensed CSP teams support you across incorporation, compliance, accounting, and beyond. Everything is coordinated through our purpose-built digital platform.

You deserve more than a chatbot and broken promises.

Serious Support for Serious Entrepreneurs

CorporateServices.com is a Singapore-based corporate services platform providing company incorporation, corporate secretarial, accounting, tax, and compliance services for businesses establishing and operating in Singapore.

When you're building something real, you need a team that can support you across every aspect of your business. No gimmicks, just reliable support for entrepreneurs who are serious about doing it right.

In a noisy market, trusted guidance makes all the difference. Low prices rarely come with high standards.

We’re Built for Reliability — Not for Investor Pitch Decks

Services

All Services You May NeedPlatform

Leading Online PlatformQuality

Satisfied CustomersPeople

Experienced CSP Teams

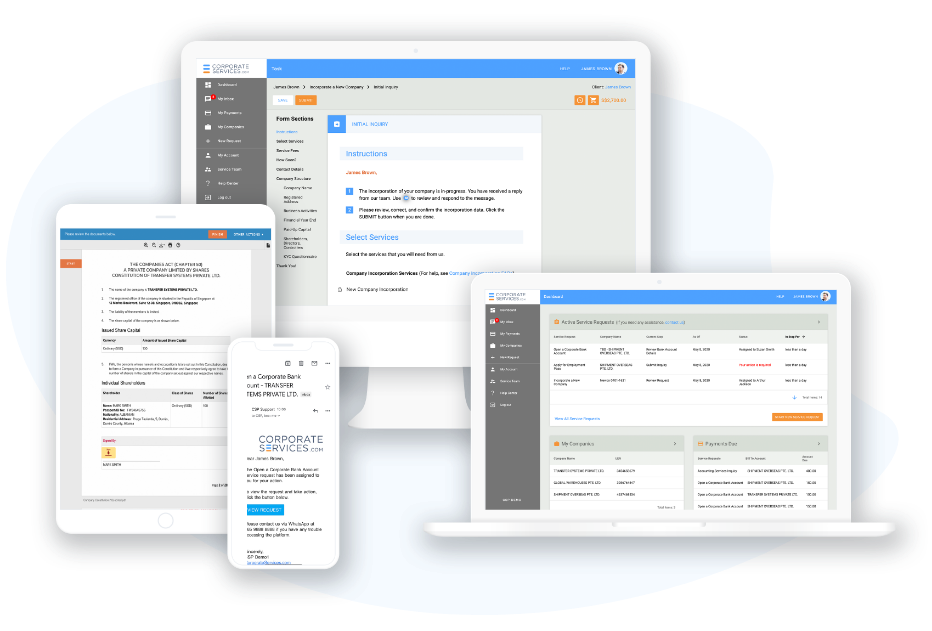

Our corporate services platform makes the company incorporation and its ongoing administration simple.

- All incorporation and compliance tasks managed by a dedicated team — just a click away whenever you need support

- Robust document management with secure e-signature support

- Purpose-built workflows that guide you step by step through each task

- Real-time tracking of ongoing tasks and submissions

- Automatic alerts for compliance deadlines and upcoming requirements

Reviews from our clients

Varun Chadha

Tirun Travel

Thank you for the efficient incorporation of our new company. In my experience with your team, all communications have been clear, thorough, and accurate...

Read more

Berner Teorica

BRT SolutionsWorking with your firm has been a pleasure. The guidance and insight you provided from start to finish made the entire incorporation process smooth...

Read more

Karen Lam

Thoughtful FoodsWe have been your clients for almost a year, and I highly commend you for the professionalism and the courteous attention that is always shown by Jacqueline ...

Read more

Company Law and Business Regulations in Singapore

Read our comprehensive guides about setting up and managing your Singapore company.

World-class partners